NEWS RELEASE 08/17/10

IASB and US FASB Publish Proposals to Improve the Financial Reporting of LeasesNorwalk, CT, August 17, 2010—The International Accounting Standards Board (IASB) and the US Financial Accounting Standards Board (FASB) today published for public comment joint proposals to improve the financial reporting of lease contracts. The proposals are one of the main projects included in the boards’ Memorandum of Understanding. The proposals, if adopted, will greatly improve the financial reporting information available to investors about the financial effects of lease contracts. The accounting under existing requirements depends on the classification of a lease. Classification as an operating lease results in the lessee not recording any assets or liabilities in the statement of financial position (balance sheet) under either International Financial Reporting Standards or US standards (generally accepted accounting principles). This results in many investors having to adjust the financial statements (using disclosures and other available information) to estimate the effects of lessees’ operating leases for the purpose of investment analysis.

The proposals would result in a consistent approach to lease accounting for both lessees and lessors—a ‘right-of-use’ approach. Among other changes, this approach would result in the liability for payments arising under the lease contract and the right to use the underlying asset being included in the lessee’s statement of financial position, thus providing more complete and useful information to investors and other users of financial statements.The boards developed the proposals after considering responses to their discussion paper, Leases: Preliminary Views, published in March 2009. In developing the proposals, the boards also considered extensive input from constituents, including more than 300 comment letters. The proposals are set out in the exposure draft Leases, which is open for comment until 15 December 2010 and can be accessed via the ‘Comment on a Proposal’ section of www.ifrs.org or on www.fasb.org. During the exposure draft’s comment period the boards will undertake further outreach activities, including public round-table meetings, to ensure that the views of all interested parties are taken into consideration before the new standard is completed.

Commenting on the exposure draft, Sir David Tweedie, chairman of the IASB, said:

The leasing industry plays an important role in many economies by helping companies manage cash flow and working capital. However, much of the estimated annual $640 billion of lease commitments fails to appear on the balance sheet of lessees, thereby giving a false impression of companies’ liabilities and gearing.Our proposals would result in better and more complete financial reporting information about lease contracts being available to investors and others.

Bob Herz, chairman of the FASB, said:

This proposal continues the progress both boards are making to improve and converge our standards in significant areas of accounting. The proposal is intended to improve the transparency of lease accounting and also decrease its current complexity. I encourage all constituents that engage in leasing transactions to provide us with your views on this important proposal.As part of their additional outreach, the boards are seeking entities that would be willing to take part, on a confidential basis, in field work to discuss and test the provisions of their proposals for lease accounting. The purpose of the field work is to assess the operationality and the costs and benefits of the proposed new standard. This exercise will be conducted during the exposure draft’s comment period.

Entities interested in volunteering should contact Aida Vatrenjak at avatrenjak@ifrs.org or Danielle Helmus at dehelmus@fasb.org by 15 September 2010.To find out more, visit the Leases section of the IASB website via http://go.ifrs.org/leases. and the FASB website via www.fasb.org. Materials available on the website include a podcast introduction to the proposals as well as a high level summary of the proposals.The IASB will hold an interactive webcast introducing the proposed standard at 10:30am London time on 18 August, and repeated at 3:30pm London time on the same day for the benefit of interested parties in different time zones.

To register, please visit the IASB website.ENDPress enquiries: Mark Byatt, Director of Communications, IFRS FoundationTelephone: +44 (0)20 7246 6472, email: mbyatt@ifrs.orgNeal McGarity, Director of Communications, FASB,Telephone : US 203-956-5347, email: nemcgarity@f-a-f.orgNotes for editors About the IASBThe IASB was established in 2001 and is the standard-setting body of the IFRS Foundation, an independent private sector, not-for-profit organisation. The IASB is committed to developing, in the public interest, a single set of high quality, global accounting standards that provide high quality transparent and comparable information in general purpose financial statements. In pursuit of this objective the IASB conducts extensive public consultations and seeks the co-operation of international and national bodies around the world. The IASB currently has 14 full-time members drawn from ten countries and with a variety of professional backgrounds. By 2012 the IASB will be expanded to 16 members. IASB members are appointed by and accountable to the Trustees of the IFRS Foundation, who are required to select the best available combination of technical expertise and diversity of international business and market experience. In their work the Trustees are accountable to a Monitoring Board of public authorities.About the FASBSince 1973, the Financial Accounting Standards Board has been the designated organization in the private sector for establishing standards of financial accounting and reporting. Those standards govern the preparation of financial reports and are officially recognized as authoritative by the Securities and Exchange Commission and the American Institute of Certified Public Accountants. Such standards are essential to the efficient functioning of the economy because investors, creditors, auditors, and others rely on credible, transparent, and comparable financial information. For more information about the FASB, visit our website at www.fasb.org.

Thursday, August 26, 2010

Monday, August 9, 2010

Monday, May 10, 2010

Critical Lease Provisions from a Tenant's Perspective

The U.S. Congressional Oversight Panel recently released their report regarding commercial real estate losses and the risk to financial stability. The objective of the report was to identify the scope of potential commercial real estate loan failures that are on the threshold to occur between now and 2014 and the risk that those failures will pose to the U.S. financial system and the public. As a tenant in a commercial real estate project it’s important to mitigate the potential risks associated with this issue by including protective provisions within your lease whether it may be up for renewal or initiating an origination.

Present Condition of Commercial Real Estate

The Panel recognized that the commercial real estate market is currently experiencing considerable difficulty for several reasons created by the financial crisis that commenced in late 2007 and the ensuing economic recession. 1. The economic turndown has resulted in a dramatic deterioration of commercial real estate fundamentals. Increasing vacancy rates and falling rental prices are affecting the ability of borrowers to make required loan payments. 2. Commercial values have fallen about 40 percent since the beginning of 20071 as a result of the decline in fundamentals. 3. Falling values result in higher loan-to value ratios, making it more difficult for borrowers to refinance. 4. The development of the commercial real estate bubble resulted in the origination of a significant amount of real estate loans based on unsound underwriting standards (i.e. overly aggressive cash flow projections and overly high levels of leverage).

1 Moody’s Investors Services and Massachusetts Institute of Technology Center for Real Estate

The Risk Between 2010 and 2014, about $1.4 trillion in commercial real estate loans will reach the end of their terms. Nearly half are at present “underwater”. The largest real estate loans losses are projected for 2011 and beyond. As can be seen from the following charts from Real Capital Analytics both the percentage and volume of defaulted loans are accelerating upward.

The Congressional Oversight Panel did not attempt to forecast the number of foreclosures or who may be most affected although the greatest concentration of risk lies within midsized and small banks which are proportionately more exposed than large banks with assets greater than $10 billion. For loans that do reach maturity, borrowers may face difficulty refinancing either because credit markets have tightened or because the loans do not qualify under new, stricter underwriting standards.

Mitigating Risk

Subordination Non-Disturbance and Attornment Agreement (SDNA)

The tenant agrees that his /her interests in the premises are subordinate to lender's interests.

The non-disturbance portion assures tenants that their rights to their premises will be preserved (“nondisturbed”) on specified conditions within their control, even if the landlord defaults on its loan and the lender forecloses.

The Attornment component of the SNDA agreement provides that the tenant will continue their obligations under the contract in the event that a new landlord takes over the contract.

· Landlord should be required to provide a non-disturbance agreement from its current and future lenders or ground lessors.

Operating Expense Payments

Either through your rent payment (as structured in a full service rent price typically associated with an office or retail lease) or as expenses that are passed through from the landlord directly from the vendor (as structured in a “NNN” lease typically associated with industrial properties), tenants are responsible for reimbursing the landlord for the expenses associated with property taxes, property insurance, managing, maintaining and operating the facility. Exclusions to this usually involve reserves set aside by the landlord to maintain the structural integrity of the building.

There are multiple risks to you as a tenant associated with these expenses:

a. Given these expenses are merely “passed through” in one manner or another to the tenant, the landlord may not be overly concerned with the competitive level of pricing secured through the vendors and readily accept price increases.

b. The proper accounting and reconciliation of these expenses may not be adequate on the landlord’s behalf resulting in billing errors to tenants.

c. Cash flow pressures in a given property may prompt landlords to increase fees that they control. (I.e. management and administrative fees).

The result of these risks is higher occupancy cost to you as a tenant.

· Landlord should be required to deliver an annual statement of actual operating expenses, certified as true and correct, within a reasonable period of time after the end of each year. Landlord should promptly reimburse tenant in the event of any overpayment.

· Landlord should not be entitled to invoice tenant for operating expenses after an outside date following the end of any year or the lease term.

· Tenant should have the right to audit landlord’s books and records relating to operating expenses. In the event of any errors, proper adjustments should be made and in the event of a signature error (3% or more), landlord should pay for the audit.

· There should be a cap on annual increases in operating expenses. The cap should be non-cumulative as opposed to cumulative. If required; the cap could apply only to controllable expenses but not uncontrollable expenses. Uncontrollable expenses should be limited to taxes, insurance and utilities only.

Given the previously mentioned decline in property values generally, determine if in fact the associated property taxes related to your facility have been adjusted to reflect the new lower values.

The CPI has been particularity low over the previous two years. Have the building expenses been growing at a significantly higher rate?

The most common billing error we encounter is capital expenditures erroneously passed through as expense items.

The Panel concluded, supported by current data, that commercial real estate markets will suffer difficulties for a number of years. Those difficulties will weigh most heavily on midsize and smaller banks but also large banks reliant on Commercial Mortgage Backed Securities (CMBS). They also could not predict with any assurance whether an economic recovery of sufficient strength will occur to reduce these risks before the large-scale need for commercial mortgage refinancing that is expected to begin in 2011-2013.

Friday, May 7, 2010

Operating Lease Moving to the Balance Sheet

By mid-2011, FASB and the IASB will likely require your leases to be booked on the Balance Sheet

This project ongoing for some time is now gathering a lot of momentum. An exposure draft is due out in Q2 of 2010 with final framework chapters expected in 2011.

Objective

The objective is to create common lease accounting requirements to ensure that the assets and liabilities arising from lease contracts are recognized in the statement of financial position.

Background

In 2006 the boards set up a joint accounting working group to address the problems users of financial statements were experiencing with the current standards. On March 19, 2009 the boards jointly issued a Discussion Paper on the changes on lease accounting. The invitation to comment period ended on July 17, 2009. This step precedes the development of an Exposure Draft and a new Statement of Financial Accounting Standards for leases by mid-2011.

Criticisms with the existing accounting model

Leasing is an important source of finance to business. Therefore, it is important that lease accounting provides users of financial statements with a complete and understandable picture of the entity’s leasing activities. The existing accounting model has been criticized for failing to meet the needs of users of financial statements in particular:

· The existence of two different models for leases (the finance model and the operating lease model) means that similar transactions can be accounted for differently reducing comparability.

· The existing standards provide opportunities to structure transactions as to achieve a particular lease classification that can be difficult for users to understand.

· Users routinely attempt to make adjustments to financial statements involving operating leases to recognize unrecognized assets and liabilities. However, the information available in the notes to the financial statements is insufficient for them to make reliable adjustments.

· Preparers and Auditors have found it difficult to define the dividing line between finance leases and operating leases in a principled way making the standard’s use difficult to apply.

Key Determinations

1 In a simple lease the lessee obtains a right to use the leased item that meets the definition of an asset and that the related obligation to pay rentals meets the definition of a liability. Consequently, the lessee will recognize:

o An asset representing its rights to use the leased asset

o A liability for its obligation to pay

2 The asset will include rights acquired under options such as renewal and purchase options.

3 The liability will include obligations arising under contingent rentals and residual value guarantees.

4 The asset and liability will initially be measured at the present value of the lease payments discounted at the lessee’s incremental borrowing rate.

5 The assets and liabilities recognized by the lessee will be based on the most likely lease term.

The factors to be considered in determining the lease term are:

· Contractual - explicit terms that could affect whether the lessee extends or terminates

a. Termination penalties

b. Bargain, discounted, market or fixed rate in secondary lease periods

c. Residual value guarantees

d. Return costs

· Non-Contractual financial factors – financial consequences not explicitly stated in the terms

e. Significant leasehold improvements lost if the lease were terminated

f. Non-contractual relocation costs

g. Lost production costs

h. Tax consequences

i. Costs associated with sourcing an alternative item.

· Business factors – non financial factors

j. Core vs. non core asset

k. Specialized vs. non specialized asset

l. Location of the asset

m. Industry practice

· The lessee’s intentions and past practice will not be considered as a factor in determining most likely lease term.

6 The lease term will be reassessed at each reporting date.

7 The incremental borrowing rate will not be reassessed

8 The obligation to pay rentals is amortized using the effective interest method over the expected lease term.

9 The right-to –use asset is depreciated on a straight-line basis over the expected lease term.

10 As a financial asset, leases will be subject to annual impairment tests.

Open Items currently being discussed

· Methodology for the annual impairment test.

· Short-term leases (less than a year) could be accounted for as operating leases.

Steps to Mitigate Risk

· Work with finance and auditors to initially measure the affected leases and create a process for ongoing evaluation.

· Identify performance metrics and related management reporting.

· Revisit existing leaseholds contracts to identify problems and opportunities under the new expected standards.

· Evaluate each leasehold asset and identify opportunities to optimize financial performance.

This project ongoing for some time is now gathering a lot of momentum. An exposure draft is due out in Q2 of 2010 with final framework chapters expected in 2011.

Objective

The objective is to create common lease accounting requirements to ensure that the assets and liabilities arising from lease contracts are recognized in the statement of financial position.

Background

In 2006 the boards set up a joint accounting working group to address the problems users of financial statements were experiencing with the current standards. On March 19, 2009 the boards jointly issued a Discussion Paper on the changes on lease accounting. The invitation to comment period ended on July 17, 2009. This step precedes the development of an Exposure Draft and a new Statement of Financial Accounting Standards for leases by mid-2011.

Criticisms with the existing accounting model

Leasing is an important source of finance to business. Therefore, it is important that lease accounting provides users of financial statements with a complete and understandable picture of the entity’s leasing activities. The existing accounting model has been criticized for failing to meet the needs of users of financial statements in particular:

· The existence of two different models for leases (the finance model and the operating lease model) means that similar transactions can be accounted for differently reducing comparability.

· The existing standards provide opportunities to structure transactions as to achieve a particular lease classification that can be difficult for users to understand.

· Users routinely attempt to make adjustments to financial statements involving operating leases to recognize unrecognized assets and liabilities. However, the information available in the notes to the financial statements is insufficient for them to make reliable adjustments.

· Preparers and Auditors have found it difficult to define the dividing line between finance leases and operating leases in a principled way making the standard’s use difficult to apply.

Key Determinations

1 In a simple lease the lessee obtains a right to use the leased item that meets the definition of an asset and that the related obligation to pay rentals meets the definition of a liability. Consequently, the lessee will recognize:

o An asset representing its rights to use the leased asset

o A liability for its obligation to pay

2 The asset will include rights acquired under options such as renewal and purchase options.

3 The liability will include obligations arising under contingent rentals and residual value guarantees.

4 The asset and liability will initially be measured at the present value of the lease payments discounted at the lessee’s incremental borrowing rate.

5 The assets and liabilities recognized by the lessee will be based on the most likely lease term.

The factors to be considered in determining the lease term are:

· Contractual - explicit terms that could affect whether the lessee extends or terminates

a. Termination penalties

b. Bargain, discounted, market or fixed rate in secondary lease periods

c. Residual value guarantees

d. Return costs

· Non-Contractual financial factors – financial consequences not explicitly stated in the terms

e. Significant leasehold improvements lost if the lease were terminated

f. Non-contractual relocation costs

g. Lost production costs

h. Tax consequences

i. Costs associated with sourcing an alternative item.

· Business factors – non financial factors

j. Core vs. non core asset

k. Specialized vs. non specialized asset

l. Location of the asset

m. Industry practice

· The lessee’s intentions and past practice will not be considered as a factor in determining most likely lease term.

6 The lease term will be reassessed at each reporting date.

7 The incremental borrowing rate will not be reassessed

8 The obligation to pay rentals is amortized using the effective interest method over the expected lease term.

9 The right-to –use asset is depreciated on a straight-line basis over the expected lease term.

10 As a financial asset, leases will be subject to annual impairment tests.

Open Items currently being discussed

· Methodology for the annual impairment test.

· Short-term leases (less than a year) could be accounted for as operating leases.

Steps to Mitigate Risk

· Work with finance and auditors to initially measure the affected leases and create a process for ongoing evaluation.

· Identify performance metrics and related management reporting.

· Revisit existing leaseholds contracts to identify problems and opportunities under the new expected standards.

· Evaluate each leasehold asset and identify opportunities to optimize financial performance.

Is it Time to "Blend & Extend", Or securing value in a soft real commercial real estate market

Many CFO’s and Treasurer’s have recently been contemplating renegotiating their lines of credit well in advance of existing maturities in response to tightened credit markets with the objective of securing sufficient liquidity for the next coming years. The phenomenon has been labeled “amend and extend”. Dependant of the individual’s outlook for availability and pricing it seems decisions are relatively split between those willing to pay some additional spread now to lock in dry powder versus those who believe that the credit markets return to functionality is under way and prefer to wait versus paying the higher pricing.

A similar but opposite phenomenon exists in the commercial real estate market. As identified in the Congressional Oversight Panels report on “Commercial Real Estate Losses and the Risk to Financial Stability”, the current commercial real estate market is experiencing the most difficulty since the early nineties. Increasing vacancy rates and falling rental prices are presenting considerable challenges for landlords and lenders of commercial real estate. On average across all property types, values in the U.S. have declined about 40% since the peak in 2007. In addition, $1.4 trillion of commercial real estate loans are maturing between now and 2014 and nearly half of those are presently under water.

As a tenant, these existing conditions make the cash flow from your tenancy more valuable today than prior to the financial crisis and ensuing economic recession. As such, many companies are employing a strategy the industry refers to as “blend and extend” which takes advantage of these conditions to generate lower rental expense today while extending the term as an offset to the landlord.

As previously mentioned, rental rates have been falling since late 2007. It is probable that if your lease commencement occurred prior to the crisis you may now be paying above current market rates. The extent of the delta will be dependant on the market and submarket in which you reside.

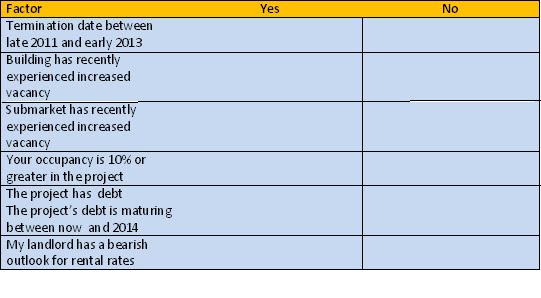

Can I as a tenant reopen my lease with the landlord to take advantage of the current lower market rental rates and lock in longer term value? The following is a list of factors which could assist you in determining whether “blend and extend” represents a viable strategy to reduce your occupancy costs:

1. Time to lease termination – your existing termination date falls between the end of 2011 and the beginning of 2013. Any earlier and the current benefits from a reduced rate are diluted. Additionally, the landlord may not be convinced you have reasonable time to relocate to a project that would offer a lower market rental rate if they declined to open negotiations. Any further out and rental rates become more difficult to project lessening a landlord’s ability to make decisions.

2. Stabilized building occupancy – if your building has been subject to increased vacancy this puts a greater emphasis on securing the cash flow from your lease term and beyond.

3. Stabilized submarket occupancy – if there is a tenant flight out of your submarket to more desirable neighborhoods within your market this also will result in a greater value on your tenancy long term.

4. Your occupancy as a percentage of the project – generally, if your occupancy represents 10% or more of the project your tenancy can wield significant weight to the project and negotiations.

5. Existing debt on the building – if debt exists on the project, the landlord must insure coverage on the debt service or perhaps face default or foreclosure which will put greater value on retaining the cash flow from your lease.

6. Debt maturity between now and 2014 – as previously mentioned $1.4 trillion in commercial real estate loans are coming due between now and 2014. Many landlords will find it difficult to refinance during this period as loan-to value ratios will have fallen outside of loan parameters and stricter underwriting requirements have been put into place. The cash flow from retaining your lease becomes of greater importance.

7. Landlord’s future market outlook (Bear or Bull) - Ultimately, the landlords willingness to open the lease and renegotiate your rental rate may be dependant on the landlords personal perception of the speed and strength of the commercial real estate markets recovery which is generally known to lag the broader economic recovery in terms of the demand for space.

To the extent your landlord is willing to open your lease and provide for a lower current rental they will generally look for an extension to the lease term as an offset to providing this concession. This becomes the “extend” component. The medium to long term generation of value is derived from calculating the effective rental rate over the new lease life relative to the rate now in place. Negotiating the escalations therefore becomes a meaningful part of the strategy.

A similar but opposite phenomenon exists in the commercial real estate market. As identified in the Congressional Oversight Panels report on “Commercial Real Estate Losses and the Risk to Financial Stability”, the current commercial real estate market is experiencing the most difficulty since the early nineties. Increasing vacancy rates and falling rental prices are presenting considerable challenges for landlords and lenders of commercial real estate. On average across all property types, values in the U.S. have declined about 40% since the peak in 2007. In addition, $1.4 trillion of commercial real estate loans are maturing between now and 2014 and nearly half of those are presently under water.

As a tenant, these existing conditions make the cash flow from your tenancy more valuable today than prior to the financial crisis and ensuing economic recession. As such, many companies are employing a strategy the industry refers to as “blend and extend” which takes advantage of these conditions to generate lower rental expense today while extending the term as an offset to the landlord.

As previously mentioned, rental rates have been falling since late 2007. It is probable that if your lease commencement occurred prior to the crisis you may now be paying above current market rates. The extent of the delta will be dependant on the market and submarket in which you reside.

Can I as a tenant reopen my lease with the landlord to take advantage of the current lower market rental rates and lock in longer term value? The following is a list of factors which could assist you in determining whether “blend and extend” represents a viable strategy to reduce your occupancy costs:

1. Time to lease termination – your existing termination date falls between the end of 2011 and the beginning of 2013. Any earlier and the current benefits from a reduced rate are diluted. Additionally, the landlord may not be convinced you have reasonable time to relocate to a project that would offer a lower market rental rate if they declined to open negotiations. Any further out and rental rates become more difficult to project lessening a landlord’s ability to make decisions.

2. Stabilized building occupancy – if your building has been subject to increased vacancy this puts a greater emphasis on securing the cash flow from your lease term and beyond.

3. Stabilized submarket occupancy – if there is a tenant flight out of your submarket to more desirable neighborhoods within your market this also will result in a greater value on your tenancy long term.

4. Your occupancy as a percentage of the project – generally, if your occupancy represents 10% or more of the project your tenancy can wield significant weight to the project and negotiations.

5. Existing debt on the building – if debt exists on the project, the landlord must insure coverage on the debt service or perhaps face default or foreclosure which will put greater value on retaining the cash flow from your lease.

6. Debt maturity between now and 2014 – as previously mentioned $1.4 trillion in commercial real estate loans are coming due between now and 2014. Many landlords will find it difficult to refinance during this period as loan-to value ratios will have fallen outside of loan parameters and stricter underwriting requirements have been put into place. The cash flow from retaining your lease becomes of greater importance.

7. Landlord’s future market outlook (Bear or Bull) - Ultimately, the landlords willingness to open the lease and renegotiate your rental rate may be dependant on the landlords personal perception of the speed and strength of the commercial real estate markets recovery which is generally known to lag the broader economic recovery in terms of the demand for space.

To the extent your landlord is willing to open your lease and provide for a lower current rental they will generally look for an extension to the lease term as an offset to providing this concession. This becomes the “extend” component. The medium to long term generation of value is derived from calculating the effective rental rate over the new lease life relative to the rate now in place. Negotiating the escalations therefore becomes a meaningful part of the strategy.

Below is a simple test incorporating the factors. The more “Yes” answers you select may indicate pursuing this strategy could yield a meaningful return.

Subscribe to:

Comments (Atom)

{kind=link}